Dorota Kosiorek, the Senior Liability Underwriter of our Polish branch draws attention to product recalls and the insurance solutions available for such cases.

More than 3,000 - that is how many products have been watched closely by regulators to verify the need for a recall in the EU in 2022. The aim of the recall is to protect consumers and prevent further damage to brand image and company reputation.

- Dorota Kosiorek, Senior Liability Underwriter, Colonnade Poland

Goods that are marketed in the EU market must meet certain requirements. Thus, companies are obliged to meet product safety and quality requirements. At the same time, in the event of any defects, companies will be obliged to take action to prevent personal injury or damage to property.

What if a product turns out to be unsafe after sales have started?

In the first instance, manufacturers must take appropriate measures to prevent risks potentially posed by their product. However, if there is a risk that the product causes a danger and endangers consumers in any way, the manufacturer will be obliged to take corrective action immediately. Sometimes, it will be necessary to inform consumers of the risk and to recall products that are already in use in order to avoid harm.

Compliance

In the European Union, product safety is ensured by the General Product Safety Directive (GPSD) 2001/95/EC to ensure that consumer products placed on the EU market are safe.

The following systems have also been established to protect consumers on the European market:

- Safety Gate (formerly Rapex) - an EU early warning system for dangerous non-food products. Its purpose is the rapid exchange of information between the European Commission and EU Member States on non-food products that may present a risk.

- RASFF - Rapid Alert System for Food and Feed. Information on food, feed and food contact materials potentially hazardous to human, animal or environmental health and the follow-up of the identification of such products is entered into this system.

Safety Gate

Over the past 10 years (2012 - 2022), there have been more than 2,000 notifications of dangerous products each year across the EU. The record year was 2014 with 2,447 notifications.

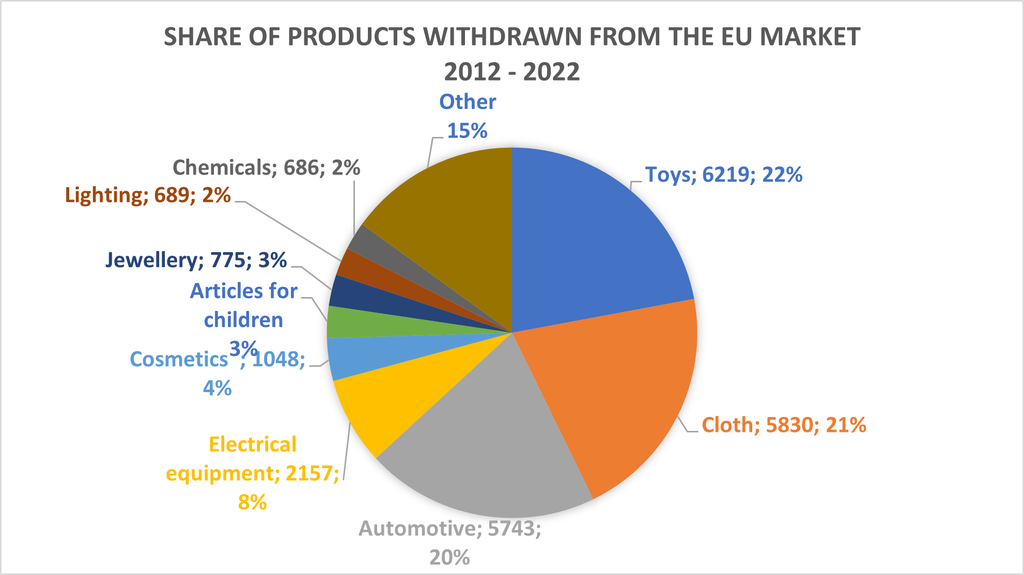

The most frequently recalled products from EU markets are shown in the chart below (based on Swiss RE Institute data for 2012 - 2022).

However, if we classify the countries from which the dangerous products originated, China is the infamous leader (more than 13,000 notifications). Germany is in second place (about 1,800 notifications), followed by the USA (about 650 notifications).

The country of origin of a defective product is not the same as the country reporting its presence.

Once a dangerous product is identified, specific action is required. Across the European Union, the recall of products endangering customer safety amounted to nearly 4,000 actions.

In addition to the statistics cited, let us also mention the largest non-food recall in history. In 2014, a defect in a car airbag manufactured by Japanese company Takata was disclosed. The airbags exploded while driving, injuring, sometimes fatally, car passengers. This defect meant that owners had to show up for servicing and replacement of the airbags. The situation affected more than 120 million vehicles, with a total recall amounting to more than US$24 billion. As a result of the incident, the company went bankrupt in less than three years.

RASFF

The last 10 years have seen an average of around 950 serious food alerts per year in the European Union alone. The strong upward trend is noteworthy. While 580 alerts were recorded in 2012, in 2022 there were 1,164.

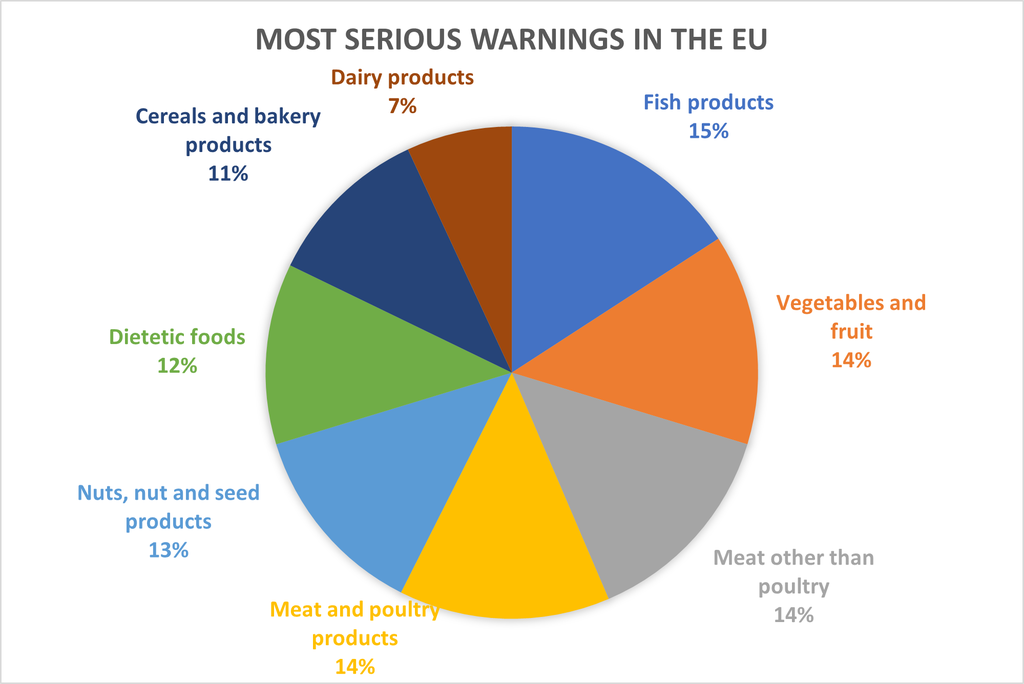

Below, the most serious alerts in the EU based on Swiss RE Institute data for 2012-2022:

Swiss Re Institute | Swiss Re - internal training materials

In 2022, the most common risks were the presence of pesticides in fruit and vegetables from Turkey, salmonella in Polish poultry and improper composition of food contact materials from China. In addition, toxins in nuts and cereals featured quite frequently in the top ten.

The food industry is also experiencing spectacular damage. The largest of these was the recall of beef in the United States. The reason was the illegal origin of the meat - mainly from diseased animals. In this case, more than 64 million tons of beef were recalled.

Risk awareness

The application of the above knowledge is extremely useful in insurance. Knowing the facts makes it possible to make both risk assessment experts and clients aware of how likely and how costly recalls can be. This is borne out by statistics that are steadily increasing.

There are many factors that can influence the need for a recall procedure. For example, failure to meet the legal standards of the country of destination or economic area (in 2022 alone, 1,514 products were stopped at EU borders that did not meet Community restrictions).

Also, products that may be considered safe in principle may carry a risk for the user. E.g. clothing, which accounts for as much as 21% of the recalls in the EU. This is quite surprising, if only because of the lack of complexity of this type of product. The main causes of risk here are usually chemicals that can penetrate the skin and clothing parts that pose a risk to children (e.g. loose parts such as cords or buttons that pose a choking/suffocation risk).

In times of high inflation, another important factor affecting product quality and safety is emerging. We are talking about reducing production costs. Lower costs are most often associated with a reduction in the quality of materials, components or assembly, and consequently an increase in the likelihood of product defectiveness.

In the context of product recalls, the role of the media and social media platforms cannot be overlooked, as they strongly influence customer awareness and behaviour. On the one hand, they are an excellent means of warning and informing about risks, on the other hand, they can wrongly create an atmosphere of danger, create unfounded fears and result in the reinforcement of a demanding attitude among consumers.

The role of insurers

The insurance market does not leave customers on their own and offers two products in case of events resulting in a product recall:

- basic insurance, Product Recall, and

- extended insurance, aimed mainly at food producers, Contaminated Product Insurance (CPI).

Product Recall focuses on covering the costs of operations to remove products from the market as such. In addition, it may cover the costs of testing, disposal or crisis consultants. This insurance can cover non-food products only, but can also be for all types of products, both food and non-food.

A broader insurance in terms of cover is CPI. Here, the insurance cover applies to food products and, in addition to the outlay required to physically eliminate the products from the market, it covers, among other things, loss of profit, coverage for the costs of re-establishing market position, the costs of re-manufacturing products to replace those withdrawn and even ransom costs in the event of blackmail to poison production.

A product recall can be initiated independently by the manufacturer, distributor or by a competent regulatory agency due to safety concerns, defects or inappropriate labelling. The purpose of a recall is to protect consumers and prevent further damage to brand image and company reputation. The recall process typically involves notifying the public, identifying the affected products or batches, providing instructions on how to return or dispose of the product and offering a refund or replacement where appropriate.

All these activities are associated with significant costs, even threatening to bankrupt the company, so it is worth considering whether transferring the risk to an insurer would be the optimal solution.